Following are highlights of the survey results:

- The great majority of American investors (73%) agree with the statement: "Firms that pay dividends tend to be predictable cash generators, and healthy dividends are a sign of financial strength."

- Three times as many investors (45%) say they increased investment in dividend-payers over the past three years as say they decreased investment in these stocks (16%).

- Investors show a strong preference for companies using dividends to return cash to shareholders, with two-thirds (69%) indicating they prefer a company to pay a dividend rather than only buying back stock.

- More investors (44%) say they prefer a smaller dividend grown annually over a large but unchanged dividend (25%) or share buybacks (19%).

- Senior investors are more likely to indicate a preference for dividends over buybacks (74%) than Baby Boomers (62%).

- GenXers also indicated a strong (70%) preference for dividends.

- The popularity of dividends is reflected in the fact that over half of investors (58%) say they currently invest in dividend-paying stocks.

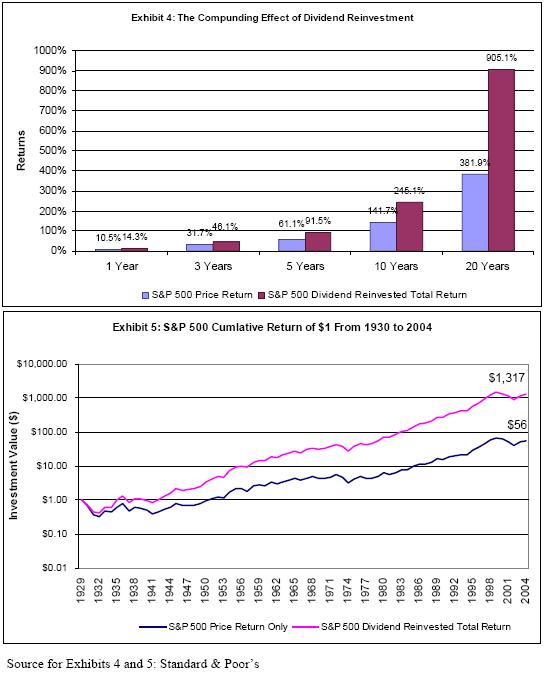

- Few investors (3%) knew that nearly two-thirds, or 64%, of the overall return from stocks as measured by the S&P 500 Index has historically come from reinvested dividends (Source: Ned Davis Research).

- Half of investors (51%) who increased investments in dividend-paying stocks over the past three years say the reduction of the tax rate on dividend income to 15% in 2003 was a factor in their decision to do so.

- Notably, 52% of GenXers--the most of any generation--say they would start investing or increase their investments in dividend-paying stocks if Congress makes the tax cut permanent.

Regarding asset preferences:

- Senior investors (34%) and Baby Boomers (31%) choose stocks as the investment they think of first for income generation, while GenXers (34%) say real estate.

- In fact, as the results of Eaton Vance's study show, investors' perception of real estate as a reliable return generator persists, despite the fact that the housing market has slowed dramatically, with September housing starts down 18% year-over-year (Source: U.S. Census Bureau News). Nearly as many investors predicted real estate would offer the best after-tax returns among major investment categories over the next five years as picked stocks (30% versus 35%).

Details about the survey:

"This summary highlights the major findings of a comprehensive telephone study among 1,209 U.S. residents 25 years and older (about 400 per age cohort: GenXers 40 and younger, Boomers 45 to 60 and seniors 65 years or older), who have over $50,000 invested in both qualified retirement plans and investments outside of qualified retirement plans (stock mutual funds, bond mutual funds, individual stocks, individual bonds, variable annuities and money market funds). This study, which represents a portrait of American investors' attitudes and practices about investing across three generations, was conducted by Penn, Schoen & Berland Associates, Inc. for Eaton Vance Corp.

This representative national study of 1,209 American investors was conducted between October 2 and November 11, 2006. By definition, all investors surveyed have a portfolio of at least $50,000, excluding housing. 71% have investable assets greater than $100,000, while one in seven have a portfolio of $1 million plus"

Source:

MSN Money

September 30, 2006

http://news.moneycentral.msn.com/ticker/article.aspx?Symbol=US:EV&Feed=BW&Date=20061130&ID=6237398

{kind=link}

{kind=link}