Market timing, i. e., when attempting to trade into our out of the market, is a difficult strategy for nearly all investors. A Barron's article written in October of last year,

The Timeless Allure of Stock-Market Timers, highlighted a few strategists' ill-timed calls and their confusion on why it did not work. The worst part of market timing is the fact the timing of getting out tends to occur near market bottoms and then getting back in the market near market tops.

Making ill-conceived market moves can reduce the growth of one's investments substantially. The below chart graphs the growth of the S&P 500 Index from 1990 through June 30, 2015. The blue line displays the growth of $10,000 that remains fully invested in the S&P 500 Index over the entire time period. The yellow line shows the same growth, but excludes the top 10 return days over the 25 year period (6,300 trading days.) By missing the top 10 return days over the 25 year period, the end period value grows to only half the value of the blue line that represents remaining fully invested.

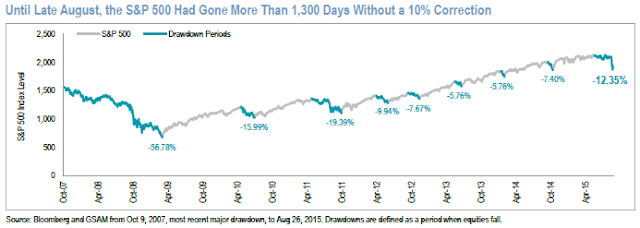

Given the market's recent pullback the calls for getting out of stocks has picked up momentum. Until this most recent pullback, the S&P 500 Index had gone over 1,300 trading days without a 10+% correction. This extended run without a 10+% correction can be seen in the below chart.

For an investor they should not get caught up in the market timing conundrum. These sell decisions often occur near equity market bottoms. Alternatively, an investor should stick with their asset allocation plan that incorporates their time horizon and risk tolerance. If the recent market pullback is jeopardizing one's retirement as a consequence of the recent downward move in equities, they should reevaluate what an appropriate asset allocation should be. The investor's asset allocation preferences should incorporate the time horizon for various buckets of assets. Shorter term investments should not be invested in equities if accessing these funds will occur over the next several years.

Timing the market may sound appealing, especially after a pullback like we are experiencing at the moment. Reducing equity exposure when the market has become increasingly volatile will certainly relieve some anxious feelings. If near term access to investments necessitates reducing equity at the moment, be sure that is the case and equity exposure is not being reduced in an effort to simply time the market. The increased market volatility experienced over the last few months is certainly more typical of equity movements and is likely to continue in the near term.