We have written many times on this blog that the simple change of one calendar day to another should not drive one's investment decisions. Just as investors are faced with the last trading day of 2013, Thursday will begin the first trading day of 2014. In spite of the opening sentence in this post, and a new year seeming to reset the clock, what is the likely market return in the coming new year?

The difficulty in predicting the market's return in 2014 is the fact one's point of reference is greatly influenced by the very strong returns achieved in 2013. The S&P 500 Index returned 32.39% in 2013. This strong market return is not a frequent occurrence; however, it has occurred in the past. The below chart is a snapshot of annual market returns for the S&P 500 Index going back to 1980. During the mid 1990's (1995 - 1999) the market was able to string together outsized gains for five consecutive years. Could 2014 be another year that rewards equity investors with strong returns?

Following are a couple of technical and fundamental market factors that are influencing

HORAN's view of the market in the coming year. Some of these factors point to a positive market return this year while others point to negative influences.

On the flip side of the high margin debt issue is the high level of short interest on S&P 500 holdings. Todd Salamone of Schaeffer's Investment Research wrote an article,

Why Stocks Could Be Set For a First-Quarter Surge, and includes a discussion on the high level of short interest as noted in the below chart. The Salamone article also details many market positives and a few market negatives that might impact the equity market in 2014.

Short covering may be a necessary factor to push equity prices higher this year. When looking at investors' mutual fund asset allocation it appears they are heavily weighted towards equities. The below chart details assets in money market and fixed income funds as a percentage of total mutual fund assets. The weighting in this non equity class is at near record lows. A major influence of this low weighting is the fact equity market returns were so strong last year; thus, pushing equity values to high levels.

In spite of the apparent low level of investor assets allocated to money market and fixed income investments, mutual fund flows would suggest the rotation out of fixed income investments into equities has only just begun as noted in the below chart. Not until 2013 did investors begin to rotate into equities. A

recent article on the Minyanville website cites

ICI data noting, "investors responded to 2013's climate by putting $160 billion of new money into equity mutual funds (investment flow data from ICI), a dramatic shift in a market that saw five straight years of outflows totaling $536 billion." One concern is the equity markets have had strong returns over the last five years and investors are just now rotating into equity investments. Individual investors could be arriving late to the bull market party, as they have a tendency to do.

From a fundamental perspective, the economy does seem to be strengthening. Real GDP in the third quarter of 2013 was revised higher to 4.1%. This is certainly a respectable rate of economic growth; however, the GDP growth rate since the end of the recent recession is below the rate of growth experienced by the economy coming out of prior recessions.

From an earnings perspective Thomson Reuters reports Q3 2013 earnings growth at about 6%. Earnings growth in Q4 of 2013 is expected to come in at 7.6%. Some of this earnings growth, however, has come by way of companies repurchasing their own stock. This has had the effect of inflating earnings per share growth since reported income is divided by fewer shares outstanding. We noted this strong buyback activity in a blog post a few weeks ago,

Stock Buybacks Continue At A Strong Pace Through The Third Quarter. The expected earnings growth rate for all of 2014 is currently estimated at 10%. Top line revenue growth is forecast at about half this growth rate at 5.7%. Importantly, we believe companies will need to generate top line growth commensurate with expected earnings growth if 2014 returns are on par with returns in 2013.

Lastly, as noted in the first chart in this post, the market can generate outsized returns for multiple years in a row, i.e., the mid 1990's. Will 2014 resemble a year similar to the mid 1990's? A common theme evident in the mid '90's period was the phenomenon of PE multiple expansion. We touched on this factor on page 2 of our

third quarter 2013 Investor Letter. The first chart below represents the period 1994 -1998. The second chart is the period 2007 - 2013.

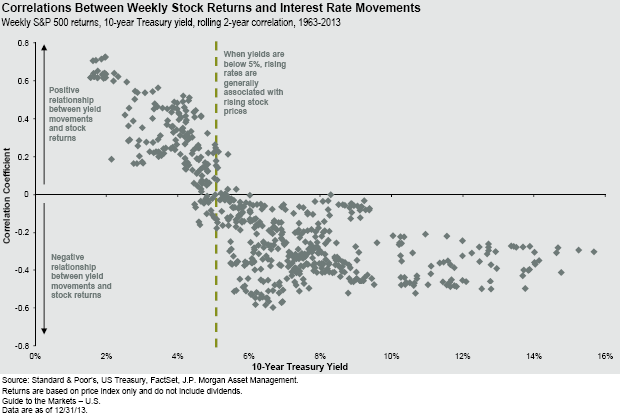

Two economic variables that are different now versus the mid 1990's is the level of GDP growth and the direction of interest rates. Multiple expansion is much easier to achieve in an environment where interest rates are falling due to how analysts value future earnings in a discounted cash flow model. In general, as interest rates decline, future earnings are valued higher in the current year period. In the mid 1990's the 10-year Treasury rate fell from 7.8% at the beginning of 1995 to a low of 4.5% before rebounding to 6.28% in 1999. This declining rate factor was a tailwind for multiple expansion. Today, the interest rate environment is completely different. In July of 2012 the 10-year Treasury yield reached 1.4% and now stands at just over 3%. This higher rate level (and the direction) makes future earnings worth less in today's discounted cash flow models and serves as a headwind to multiple expansion. Multiple expansion can still occur when the economic growth rate is picking up steam though. This occurs because investors expect company earnings to grow more quickly as the economic climate improves. Certainly the third quarter GDP report is suggestive of this. In 2014, a faster growing economy will be an important factor in order to generate outsized returns in the equity market.

What is evident from the above factors is the fact the data is mixed in regards to technicals as well as fundamentals. This mixed type of data has been prevalent since the end of the financial crisis and is likely a factor that has prevented investors from appearing to go 'all in' on stocks. There are a number of other factors we are reviewing at

HORAN Capital Advisors in assessing the markets in 2014. For our readers though, we hope this provides you with a few of the potential influences that may impact the market in 2014. We will provide additional insights in our upcoming quarterly investor letter. We wish all of our clients and readers a healthy and prosperous New Year!