The market has interpreted recent commentary from the Fed that quantitative easing (QE) may be nearing an end. This type of thinking from market participants has led to a significant sell off in many fixed income investments as well as yield focused equities and ETFs.

The negative impact with the price performance of many of these investments that have fixed income qualities has been exacerbated by the fact the underlying investments in some of these ETFs are highly leveraged in and of themselves. In the ETF MORT, one of the top holdings is Annaly Capital Management (NLY). NLY is leveraged about 9 to 1, debt to equity. Consequently, as the cost of borrowing rises, the amount of income payable to investors declines as interest cost increases. Additionally, as rates rise, the value of the mortgages that make up the assets of these mortgage type REITs (mREITs) declines. Also, some higher yielding investments borrow in order to purchase additional assets, like Nuveen's Premium Municipal Income Fund 2 (NPM) that currently borrows nearly 34% of its underlying assets to purchase additional investments.

Leverage is a double edged sword and works great when interest rates are falling. However, as rates begin to rise, leverage can really harm one's investment returns. At HORAN, we historically steer clear of leverage within our investments because of the outsized negative impact on performance when interest rates turn higher. As the below chart of the 10-year Treasury shows, it does not appear interest rates can fall much further.

Over time, as investors approach and enter into retirement, fixed income is often viewed as the stable portion of one's investment portfolio. Today though, central banks around the globe have implemented monetary policies that have pushed interest rates to near record lows. Does this artificial stimulus then make fixed income a not so safe investment asset class?

From a prudence point of view, some factors investment advisors inquire about of their clients is an appropriate investment objective, time horizon for the investment funds and risk tolerance. Much thought should certainly go into these decisions so an appropriate asset allocation and investment strategy can be developed. The ultimate asset allocation goal often leads advisors to talk about risk adjusted returns and possibly modern portfolio theory (MPT). The MPT discussion likely will not occur in those exacts words, but some form of generating returns by assuming less risk will be a general theme of the discussion. The advisor's goal in the discussion is to develop a portfolio that lies on the so-called efficient frontier.

We have written a number posts on the limitations of MPT, (here, here and here) and increasingly believe the artificial distortions unfolding in the fixed income markets could provide further risk to investors that rely strictly on MPT. In a recent introductory paper on Modern Portfolio Theory and authored by Donald R. Chambers, he states,

"...In the wake of difficult times such as the financial crisis that began in 2007, the concept of market efficiency is sometimes criticized. However, while no market is perfectly efficient, the evidence suggests that behaving as if markets were highly efficient provides investors with a solid approach (emphasis added)."

Simply having a "solid approach" does not necessarily lead to higher returns though. Many managed futures funds are constructed using a solid approach. Morningstar reports the average one year return for the managed futures category is a negative 4.73% as of May 24, 2013. The best returning fund over one year reported a return of 9.22%. This compares to the return for the S&P 500 Index of nearly 28%. As a category, the managed futures funds achieved the return with half the risk of the market or S&P 500 Index. For investors then, do you prefer this 9.22% return or the 28% return knowing the market portfolio assumed 50% more risk. Hindsight is a wonderful perspective.

A recent interview by Citadel strategist, Maarten Ackerman, contains a pertinent discussion on MPT and the efficient frontier. The risk for bond investors in this low interest rate environment is evident in the discussion with Ackerman. Ackermann continues to have confidence in MPT; however, discusses the risk inherent in bonds in this low interest rate environment. One weakness in MPT is the use of past returns and risk. Using potential

returns and potential risks certainly is a preferred approach. He mentions an alternative to bonds is higher yielding high quality dividend paying stocks. In my view, stocks are not bonds. This chasing of yield has pushed the valuations of the defensive stocks to potentially stretched levels as noted in several earlier posts.

For investors, keep in mind that during financial market stress, the correlation of most assets classes moves to near 1.0, i.e., they all go down together. Additionally, these are unique times with central banks flooding economies with liquidity. One technical investor commentary I follow is Charles Kirk of The Kirk Report. He has noted on many recent occasions that the "technical" trading setups are not unfolding as one would have expected in the past. The artificial stimulus activity from central banks could be playing a role in this. One quote scrolling through our Horan website is from Sir John Templeton, "The four most dangerous words in investing are: 'this time it's different.'"

Maybe it is different this time and another event transpires that highlights the weakness in Modern Portfolio Theory.

Standard & Poor's notes in a recent report on Earnings Yield By Sector that seven of ten S&P 500 sectors have earnings yields greater than their long term averages. As of mid-May, the S&P report notes,

"the earnings yield on the S&P 500 was 5.4% (based on trailing GAAP EPS through Q1 2013), and nearly three times as high as the 1.9% yield on the 10-year Treasury bond. The last time the EPS yield was this far above the 10-year note yield was in 1955....Common wisdom holds that if stocks are yielding a lot (in EPS) relative to bonds (in interest), stocks are more attractive than bonds."

The S&P research report contains an analysis of the historical yield relationship and the subsequent 12-month performance achieved by the Index.

Another interesting aspect of the report is the average sector earnings yield relative to the 10-year Treasury Note. The three sectors that have earnings yields to 10-year Treasury Note multiples that are currently below their average are consumer staples, utilities and telecommunications. These three sectors are ones that have had the strongest performance this year through April 26th as noted in our post, Sector Rotation Underway. Since April 26th though these same three sectors have had the worst performance.

Some of the sectors with the best performance since April 26th are those that have the highest earnings yield relative to the 10-year Treasury note yield.

"since stocks are yielding nearly three times in EPS what bonds are yielding in interest, history suggests that stocks may be the more attractively valued asset class. And since the cyclical sectors are trading at a higher premium to their normal EPS-to-bond yield multiple than the defensive sectors, the recent rotation into cyclical sectors at the expense of the defensive ones is a trade that appears to us to have some sustainability."

For investors, although stocks appear appear to be a more attractive investment versus bonds, the summer months historically have been a weak period for equities.

Source:

Earnings Yield By Sector

by: Sam Stovall, Chief Equity Strategist

Standard & Poor's

May 14, 2013

http://us.spindices.com/documents/commentary/20130514-sector-watch-eps-yields.pdf?force_download=true

Today's release of AAII's Investor Sentiment Survey saw bullish investor sentiment increase 10.5 percentage points to 49.0%. This reading is right at the average plus one standard deviation level. The bull/bear spread widen to +27.4%. The weekly reading can be volatile so looking at the 8-week moving average smooths some of this volatility. This week's 8-week average is reported at 33.7%, up from 32.3% last week.

In the final second of trading on Friday, Anadarko Petroleum Corp. (APC) goes from a $90 stock and trades down to $.01, that is a penny a share before closing at $90.03. I am sure some buyers (computers) thought they were fortunate to pick up APC at one penny. On the contrary, the NYSE canceled trades executed below $87.56 per share.

As the market continues to seemingly move higher every day, investor complacency appears to be on the rise. The recent CBOE equity put/call ratio is at a low level of .50. Like other sentiment indicators, this measure tends to be more accurate at extremes. On April 20th we wrote about the elevated put/call ratio and wondered if the market was excessively bearish. Since the time of that post, the market has advanced over 7%.

Additionally, fixed income assets as a percentage of all mutual fund assets recently began to decline. Are investors now warming up to equities in spite of the strong advance that has occurred year to date? On the other hand, given the low level of interest rates, bond investors are having a difficult time finding fixed income assets that provide adequate yield without taking on maturity and/or credit risk. Income yielding stocks seem to be the bond investors new bond substitute.

Recent economic news has not been great or not as bad as economist had expected. The Empire State Manufacturing Index was below expectations, housing starts lower than expectations and industrial production lower than expectations. The employment numbers showed an improvement last week; however, it is difficult to gauge whether it is because people continue to drop out of the work force (declining participation rate) and other non favorable factors.

This is certainly a difficult point in the market cycle for investors to navigate. One thing the market does like to do is one, prove the consensus wrong and two, climb the proverbial "wall of worry."

Morningstar recently reported the number of bond funds buying or holding stocks is at the highest level in 18 years. The below chart from Charles Schwab details data over the last ten years. Schwab/Morningstar note the percentage of bond funds holding equities has remained stable over this time period though. Nonetheless, more bond funds are buying equities in an effort to find higher yielding securities than currently available from bonds.

In addition to bond funds jumping into dividend yielding stocks, Schwab reported the following from a survey of the central banks around the globe:

"Last month, Central Bank Publications and Royal Bank of Scotland Group Plc conducted a survey of 60 central bankers. Nearly 25% of respondents said they own stock shares or plan to buy them. The Bank of Japan, featured heavily in the news recently and holder of the world's second-largest level of reserves, said it will more than double investments in stock exchange-traded funds by 2014. The Bank of Israel bought stocks for the first time last year, and the Swiss National Bank and Czech National Bank have upped their holdings to at least 10% of reserves.

Of the 60 banks surveyed, 14 said they'd already invested in stocks or would do so within five years. In fact, this is the first time ever the question about stocks has been in this annual survey.

Behind the heightened interest in stocks are growing central-bank reserves requiring increased diversification. In US dollar terms, the four largest central banks have expanded their balance sheets to more than $13 trillion, compared to only $3 trillion 10 years ago. Most central banks have had heavy and consistent reliance on fixed-income securities, but with yields low (and falling) in many countries, keeping all reserves in fixed income risks a declining value of reserves.

However, 70% of the central banks in the survey (including the US Federal Reserve) indicated that stocks remain "beyond the pale." A few central banks, including the Fed and the Bank of England, have no mandate to purchase stocks directly.

Jim O'Neill, chairman of Goldman Sachs Asset Management, weighed in: 'I don't think people should worry about (central banks owning stocks). Frankly, it makes a huge amount of sense in a world of floating exchange rates and such incredible opportunity, why should central banks keep so much money in very short-term, liquid things when they're not going to ever need it?'"

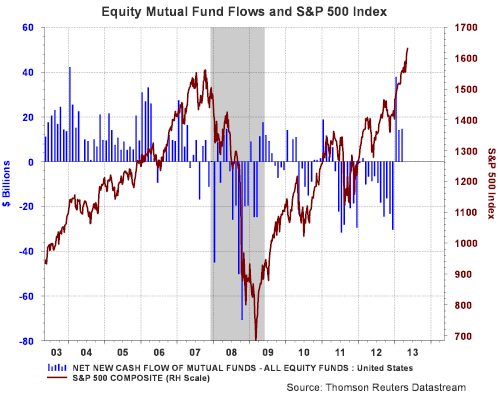

Not much seems able to restrain the strength of the bull market in U.S. equities. On a year to date basis the S&P 500 Index is up 15.43%. The advance has finally drawn investors into equity mutual funds as reflected in positive equity mutual fund flows the first three months of the year.

The positive market results continue to keep the S&P 500 Index in a positive uptrend channel that began in the middle of November of last year. Aside from the fact company fundamentals and valuations look reasonable, at least not overvalued, higher equity prices could continue to unfold. However, we have noted in several recent posts the rotation that has occurred of late out of the more defensive sectors into the more cyclical ones.

Because of the significant amount of artificial stimulus being pumped into the global economy by most central banks around the world, we believe investors need to have a heightened focus on the underlying technical aspects of the market in order to gain insight into potential market turning points. No one technical indicator is the panacea that will predict the market's future direction. One indicator useful to evaluate for the market and/or individual stocks is the Money Flow Index (MFI). This index is a variation of the Relative Strength Index (RSI). The StockCharts.com website provides the following definition of MFI:

"The Money Flow Index (MFI) is an oscillator that uses both price and volume to measure buying and selling pressure. Created by Gene Quong and Avrum Soudack, MFI is also known as volume-weighted RSI. MFI starts with the typical price for each period. Money flow is positive when the typical price rises (buying pressure) and negative when the typical price declines (selling pressure). A ratio of positive and negative money flow is then plugged into an RSI formula to create an oscillator that moves between zero and one hundred. As a momentum oscillator tied to volume, the Money Flow Index (MFI) is best suited to identify reversals and price extremes with a variety of signals."

"The Money Flow Index is a rather unique indicator that combines momentum and volume with an RSI formula. RSI momentum generally favors the bulls when the indicator is above 50 and the bears when below 50. Even though MFI is considered a volume-weighted RSI, using the centerline to determine a bullish or bearish bias does not work as well. Instead, MFI is better suited to identify potential reversals with overbought/oversold levels, bullish/bearish divergences and bullish/bearish failure swings (emphasis added). As with all indicators, MFI should not be used by itself. A pure momentum oscillator, such as RSI, or pattern analysis can be combined with MFI to increase signal robustness."

As the below charts display, the weekly chart of the market and the MFI are showing divergence. A weekly time period is used in order to smooth out the potential day to day market variations. On the daily chart, the MFI trend is positive; however, the index recently rose above the overbought area of 80 on the chart. Also, market volume has been in a steady decline since late 2011 and has not picked up in spite of positive equity fund flows as noted in the first chart in this post.

At HORAN, we do remain positive on the market, but believe some consolidation could occur and would be healthy for the performance potential through the balance of the year. Our focus has been to reduce or sell some of the holdings in the defensive sectors and build or add to positions in the more cyclically exposed sectors that have underperformed this year, and over the last year for that matter. One stock we trimmed recently was Johnson & Johnson (JNJ). We trimmed the holding for more than technical reasons, but looking at the chart with the MFI overlay, it does show some potential stock weakness ahead when looking at just the MFI.

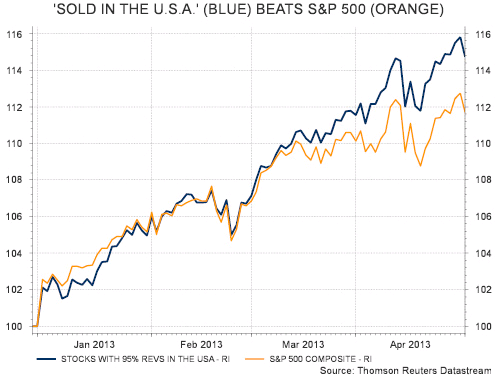

In a recent AlphaNow report from Thomson Reuters, it shows U.S. companies that generate a majority of their revenues from the U.S. are outperforming the broader market S&P 500 Index. The report highlights that 150 companies/stocks generated at least 95% of their revenues within the USA and outperformed the S&P 500. On a 2013 year to date basis (through May 1), they note their total return beat the S&P 500: 15% vs. 12%, and 31% to 21% in the past two years.

The report also notes, "The three top overweights come in sectors which have all outperformed so far in 2013 (see chart) – financials (+13% overweight), telecom services (+11%) and utilities (+10%). That’s before adding in consumer discretionary (+2% overweight) which is the second best performing sector as of May 2." Of late though, much has been stated about the potential rotation underway out of these more defensive sectors and into the more cyclically oriented ones. Investors need to be on guard about chasing past returns.

We noted in a post a week and a half ago that the market's defensive sectors have been the main driver of the S&P 500 Index's strong performance this year. In this earlier post, Sector Rotation May Be Underway, we noted investors may be rotating out of the defensive sectors and into the more cyclical ones. In that regard, J. C.Parets of All Star Charts wrote an interesting article showing the more cyclical sectors recent strong performance vs. the staples sector is retesting resistance for the fourth time in two years. This number of retests has historically been a bullish indicator and could be for cyclicals in this now. The question is whether this rotation into cyclicals can be sustained and drive the market to further highs.

Ten years ago Standard and Poor's released its Equal Weighted S&P 500 Index (EWI). Since that time a number of index firms have created equal weighted ETFs that investors are able to invest in directly. In S&P's recently released white paper, 10 Years Later: Where In The World Is Equal Weight Indexing Now?, they cover a great deal of the historical data on the equal weighted index relative to the more common market cap weighted S&P 500 Index. Due to the cap weighted nature of the S&P 500, one obvious characteristic is the EWI S&P 500 is more heavily weighted in the smaller capitalization stocks and underweighted in the large cap stocks of the S&P 500 Index. Because of this factor, S&P demonstrates the equal weighted index does have a tendency to outperform more frequently in up markets than in down markets and the EWI does carry a higher beta.

Given the emergence of technology and the tech sector leading up to the technology bubble in 2000, one might believe performance differences between equal weighted and cap weighted indices is due to the differing sector weights. However, one must keep in mind the sector weighting within the EWI is determined by the number of companies that make up the overall index. As noted by S&P,

"Since 1999, the S&P 500 EWI has been consistently overweighted materials, consumer discretionary and utilities, and underweighted energy, health care and telecommunication services relative to the S&P 500. However, for other sectors the situation has varied considerably over time. In fact, even for sectors for which the S&P 500 EWI has been consistently overweight or underweight, the difference in concentration between the two indices has altered significantly.

Throughout the history, the largest change in the relative sector weights of the two indices has been in the information technology (IT) sector, mainly due to the change in the sector weights of the S&P 500 itself. During the technology bubble in the late 1990s, the IT sector weight of the S&P 500 increased to 33% in March 2000 from 13% at the start of 1998. Correspondingly, the S&P 500 EWI went from being underweight in the sector by less than 3% to being underweight by more than 20% in the same period. This has a very important implication that explains the different performance of the S&P 500 EWI relative to the S&P 500..."

S&P's paper does indicate the performance differences are more attributable to selection effects than allocation effects though.

A recent example of this selection impact can be seen in the below chart comparing the S&P cap weighted and equal weighted (RSP) performance relative to Apple's (AAPL) stock price performance. RSP is the Guggenhiem S&P 500 Equal Weighted ETF. Apple remains the largest holding in the cap weighted S&P 500 Index and its significant underperformance since mid November has contributed to the cap weighted index underperforming the equal weighted index.

For investors then, an equal weighted approach may not result in outperformance on an every year basis; however, it has proven to outperform over longer time frames. Additionally, the EWI is rebalanced on a quarterly basis, thus, leading to a strategy that results in selling high and buying low.

In this low interest rate environment, investor search parameters on Google indicate investors have a propensity for dividend paying stocks at this point in time. Last week we noted in our post, Sector Rotation May Be Underway, that the defensive sectors in the S&P 500 Index generated strong outperformance versus the more cyclical sectors this year. A common characteristic of these defensive sectors is they comprise some of the better dividend yielding stocks. A caution for investors is many of the stocks within the defensive sectors are trading at historically high valuations on a price to earnings basis.