Below is a list of the most read blog articles in each month during 2017. One interesting commonality for some of the top posts is the fact the ones focusing on investor sentiment tend to gain higher levels of readership. Sentiment is one important market factor we monitor on a fairly regular basis. Secondly, some prior articles seem to remain applicable as 2018 is set to begin. For example, articles like Market Pullbacks Should Be Expected and The S&P 500 Index Is Expensive and Has Been So Since The Early 1990's are certainly timely even today.

Our firm's bullish equity stance in 2016 and 2017 has certainly rewarded our clients. We are in the midst of finalizing our Winter Investor Letter which will contain some of our firm's thoughts on the coming year.

To our clients and readers, we wish all of you a Healthy and Prosperous New Year.

Second Longest S&P 500 Rally Since 1932 - January 25, 2017

Recent Outperformance Of Low Volatility A Sign Of Risk Off Ahead? - February 12, 2017

Time To Reduce One's Equity Exposure? - March 1, 2017

Widespread Bearishness Indicating Market Nearing A Turning Point? - April 14, 2017

The Unfortunate Rise Of The Misleading 'Scary Chart' Comparisons Again - May 29, 2017

Market Pullbacks Should Be Expected - June 26, 2017

Strong Earnings Growth And Favorable Valuations Lead To Weak Stock Returns - July 22, 2017

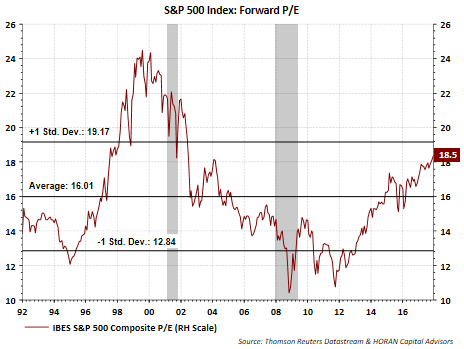

The S&P 500 Index Is Expensive And Has Mostly Been So Since The Early 1990's - August 5, 2017

Stocks Need Some Healthy Competition - September 16, 2017

Citgroup Economic Surprise Indices Have Little Bearing On Equity Market Performance - October 15, 2017

Individual And Investment Manager Sentiment Is Diverging - November 2, 2017

If Cash Is King - December 19, 2017