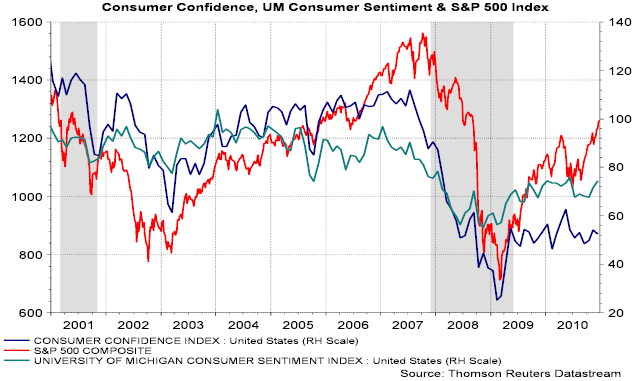

Much is made of the fact that investors should allocate some of their investment portfolios to emerging market economies. This makes sense from the standpoint the emerging economies of the world have been experiencing stronger economic growth versus the developed economies.

|

| From The Blog of HORAN Capital Advisors |

From a cautionary perspective though, investors need to be aware of the strong returns already achieved in the emerging markets over the last ten years. From a performance perspective, the emerging markets' 10-year annualized returns are around 13% (MSCI Emerging Markets Index) versus the 10-year annualized return of the S&P 500 Index of around 1%.

On a prospective basis, the emerging economies are still expected to achieve economic growth rates that are higher than those of the developed economies. A recent article by T. Rowe Price, The Decade Ahead, highlights economic growth rates out through the end of 2020. Certainly a long time frame, but the graph to the right points to the opportunities in these emerging economies based on their projected growth rates.

At HORAN Capital Advisors, we do have an overweight to the emerging markets versus our baseline allocation. Also included in our investment philosophy is to invest in U.S. or foreign multinational companies that do, or intend to, derive a large part of their revenue from emerging market economies.

Lastly, on a shorter time frame, two years, GDP growth in the developed countries is expected to grow 3.5%. And GDP growth in the developing economies is projected to grow 25%% through 2012.

Before investors allocate investment funds to the emerging markets, they should conduct there own research. A number of the emerging countries are attempting to slow their faster growing economies by pursuing a tighter monetary policy. On a short term basis the tighter policy could reduce growth rates and have a short term negative impact on market returns.

On a prospective basis, the emerging economies are still expected to achieve economic growth rates that are higher than those of the developed economies. A recent article by T. Rowe Price, The Decade Ahead, highlights economic growth rates out through the end of 2020. Certainly a long time frame, but the graph to the right points to the opportunities in these emerging economies based on their projected growth rates.

At HORAN Capital Advisors, we do have an overweight to the emerging markets versus our baseline allocation. Also included in our investment philosophy is to invest in U.S. or foreign multinational companies that do, or intend to, derive a large part of their revenue from emerging market economies.

Lastly, on a shorter time frame, two years, GDP growth in the developed countries is expected to grow 3.5%. And GDP growth in the developing economies is projected to grow 25%% through 2012.

Before investors allocate investment funds to the emerging markets, they should conduct there own research. A number of the emerging countries are attempting to slow their faster growing economies by pursuing a tighter monetary policy. On a short term basis the tighter policy could reduce growth rates and have a short term negative impact on market returns.

|

| From The Blog of HORAN Capital Advisors |