Consuelo Mack of

WealthTrack recently aired two interview segments that focused on women and their investing and retirement needs. American women control $8 trillion in assets and this figure is expected to grow to $22 trillion by the end of the decade. Yet the traditional wealth management approach doesn’t necessarily work for women’s needs. In the first video Consuelo Mack's guests, Morgan Stanley’s Ami Forte, and GenSpring’s Senior Strategist, Jewelle Bickford, discuss how women can start taking ownership of their financial power.

Importantly, only 1 in 5 women have determined how much money they will need in order to maintain their lifestyle in retirement. From a longevity perspective, on average women will live 5 years longer than a man. Today, 75% of the population age 85 years old or over is comprised of women.

In the second video below (Part II), Consuelo Mack notes, "Women worry about becoming bag ladies in their old age and men focus too much on performance numbers, which isn’t always the best way to plan for the future." Her guests are Mary Beth Franklin, a contributing editor for InvestmentNews as well as an expert on social security, and Erin Botsford, founder and CEO of the Botsford Group, where they explain why women are so different from men in their approach in planning for the so-called “Golden Years”.

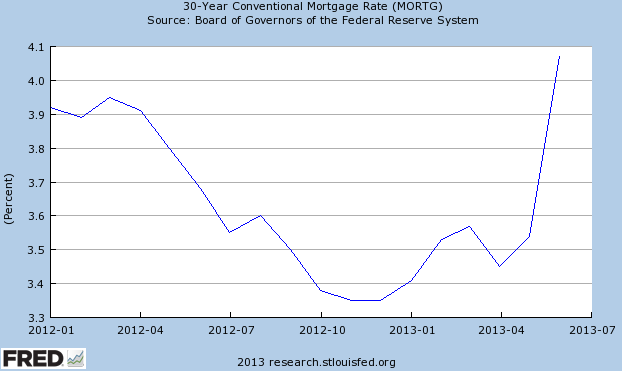

In the first video the guests note investments today are more than simply allocating ones investment funds between stocks, bonds and cash. At HORAN our investment approach incorporates other asset classes as well. Our alternative allocation is an effort to enhance a client's investment returns without taking the same level of risk as equities, but generate a return better than fixed income or bonds. As Ami Forte notes in the first video, bonds were traditionally known as safe asset class, however, the recent rise in interest rates has exposed just how risky the bond asset class can be.