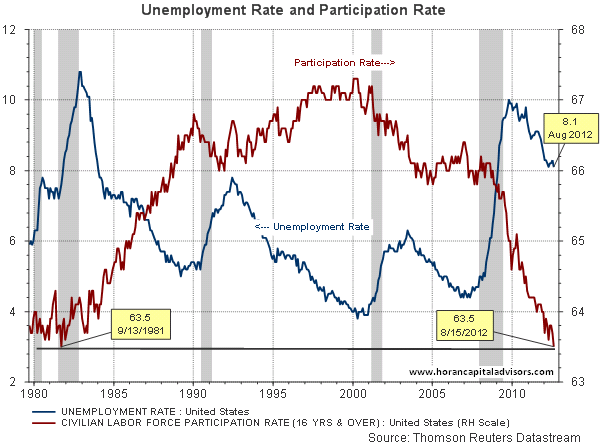

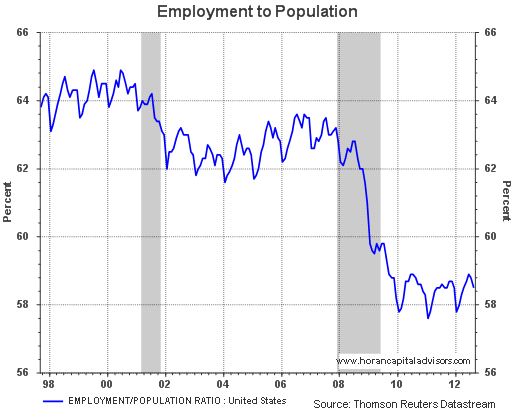

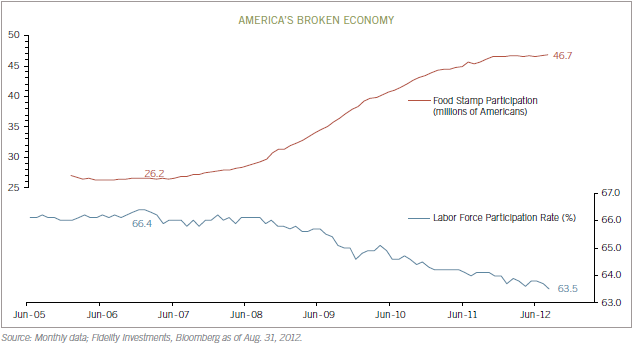

Central banks around the world are doing all they can to pump liquidity into their respective economies. To date though, their actions are having limited effectiveness when it comes to improving economic growth. One consequence of the slow growth in the U.S. is the dramatic increase in food stamp usage. The increased food stamp usage also seems to translate into a lower labor force participation rate as well.

|

| From The Blog of HORAN Capital Advisors |

Source:

Boxing Match: Central Banks vs. the Economy

Fidelity Viewpoints

By: Jurrien Timmer, Portfolio Manager

September 16, 2012

https://news.fidelity.com/news/article.jhtml?guid=/FidelityNewsPage/pages/fidelity-central-banks-vs-the-economy&topic=economy