In December the Federal Reserve indicated they would begin reducing their bond buying (taper) at the rate of $10 billion per month starting in January. The bond market had certainly factored in this announcement and had expected this outcome to be announced at an earlier Fed meeting. The direct consequence of the taper discussion and ultimately its implementation is interest rates rose dramatically in the last two quarters of 2013. As the below chart shows, the 10-year Treasury yield rose from 1.61% in May to 3.03% at year end.

|

| From The Blog of HORAN Capital Advisors |

A result of this increase in interest rates is bond prices fell with most bond or fixed income categories generating negative returns for investors in 2013. If bonds are not a favored investment in a rising interest rate environment, and if rates trend higher in 2014, what is the likely impact of higher rates on stock prices?

The table below is provided courtesy of T. Rowe Price and from their Winter newsletter. The table details equity performance during periods of rising rates going back to 1970. During most of the rising interest rate periods, equity prices moved higher during this period of time.

|

| From The Blog of HORAN Capital Advisors |

One reason equities tend to move higher as rates rise is the fact rate increases are generally associated with an improving economic environment. The higher rates can ultimately hinder economic growth; however, at the onset of increasing rates, stocks tend to shrug off the higher interest rate move. Page 16 of the T. Rowe Price Report is a worthwhile read and goes into greater detail on this. If rates are increasing due to inflationary factors, a different outcome may occur. We wrote about stock prices and inflation in an earlier post, Where To Invest In An Inflationary Environment, that readers may find of interest as well. At this point in time we do not believe the stars are aligned that will give us significant inflation near term.

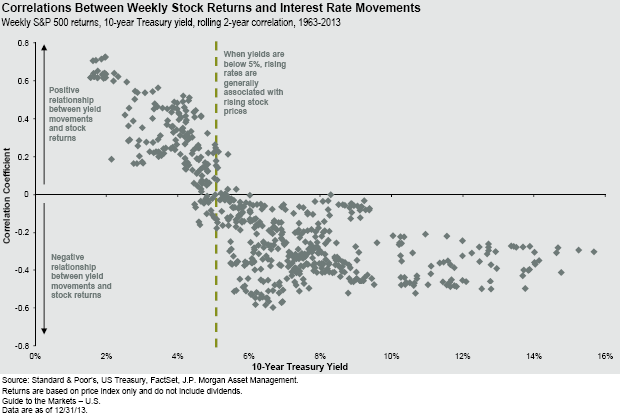

Lastly, one chart that made the rounds within the investment community recently was the one below showing equity correlation in a rising interest rate environment. This chart comes from J.P. Morgan's first quarter 2014 Guide To The Markets (page 12). The chart indicates when the rate on the 10-year treasury is rising from a level below 5%, stocks are positively correlated to the rate move, i.e., rates and stock prices move in the same direction. When rates are rising from a very low level, it is an indication rates are simply getting back to a more normalized level and this level does not inhibit economic growth. When rates are rising above 5%, this may occur because inflation is becoming an issue, the economy is beginning to grow too rapidly, etc. and this higher rate level could slow economic growth; thus, negatively impact corporate profit growth.

|

| From The Blog of HORAN Capital Advisors |

For investors, the Fed seems certain to begin tapering QE. If this reduced QE level does cause rates to rise further, bonds are likely to be a more challenging investment versus stocks in the coming year. We do believe if the tapering does cause a broader market disruption, the Fed will be quick to turn on the QE pump again. It seems the central banks around the world are addicted to this stimulus activity. An interesting perspective on this activity was discussed in the WealthTrack interview with Ed Hyman that we posted yesterday.

2 comments :

One of the causes of 2008 - 2009 crash was rising interest rate. Is it different this time?

W,

You are correct that the Fed Funds rate began to rise from 1% in 2004 to over 5% in 2006. I do think it is worthwhile to view the rate rise in conjunction to what was occurring in the economy at that time. Economic activity, and specifically housing speculation, was taking place then versus what we have today. I believe the Fed's desire to reduce QE, with the counter effect that reduced QE will generate higher interest rates, is the Fed's desire to get interest rates back to a more normalized level. Certainly all the QE/stimulus provided by the Fed and its attempt to reduce QE is really an experiment that no one really knows what the outcome will be. From our firm's perspective we do believe the economy is slowly gaining strength at best, with a worst case of bump along the bottom economic growth, not a contraction though.

Post a Comment