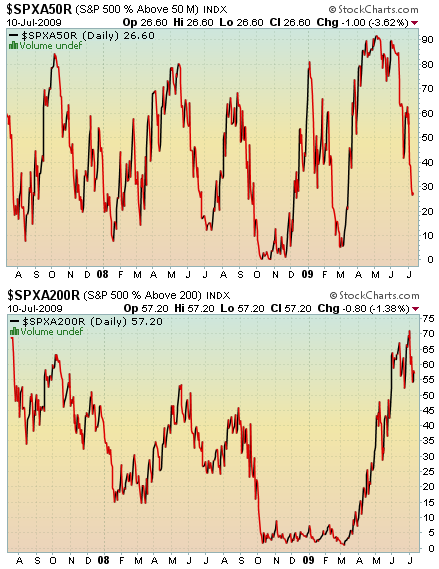

I continue to believe investors are in denial regarding the sustainability of this market advance and for good reason. Over 85% of S&P 500 stocks are trading above their 50 day moving average. As noted by the white circle near the top of the chart though, the market can continue to move higher while the percentage of stocks trading above their 50 day trends sideways.

As I have noted in earlier posts, the below chart was first publish in 1991 by technical analyst Justin Mamis in a book titled The Nature of Risk.

As the chart of the S&P 500 Index shows below, the resistance level is around S&P 1005. This was the level achieved in early November 2008 and corresponds to the market rebound from the panic phase in the above chart.

The caution is this analysis is strictly technical and the market could be topping out at the anxiety phase. Nonetheless, it appears we are past retesting the March lows.

Fundamentally, recent earnings reports have shown nearly 50% of companies reporting earnings have beat analyst estimates. This might not say much given analyst normally over estimate earnings at market tops and underestimate earnings at market bottoms. What if analyst under estimate earnings at the bottom of the market, maybe the second quarter does represent trough earnings. What is necessary now is top line revenue growth on a year over year basis.

Many companies have right sized their companies to operate at levels not seen since 2003 or 2004. Using one of these years as a reference point, then when will the year over year bar be low enough that top line revenue growth will show year over year growth? For some companies this positive year over year revenue growth bar could be realized in the 4th quarter this year and for others the first quarter of 2010. As the market tends to be a leading indicator, the market's recent advance may be telegraphing this potential scenario.

Individual investor sentiment continues to remain on the cautious side. The

American Association of Individual Investors reported that bullish investor sentiment did increase to 37.60% versus last week's bullishness reading of 28.68%. However, the bull/bear spread remains at a negative 5%, an improvement from last week's spread of negative 18%. Prior market tops have occurred at spreads above 30%. Since the sentiment reading is a contrarian indicator and individual investors are not overly bullish, further market advances could be on the near term horizon.