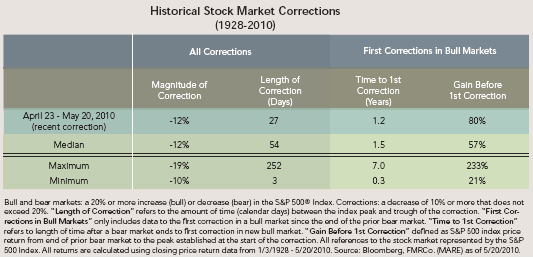

If an investor maintains any cash in a money market/savings account today, they know interest rates are at levels approaching zero percent. Consequently, it does not seem as though rates can go much lower. When (not if) interest rates do begin to trend higher, be it 6, 9 or 12 months from now, the impact on the price or value of bond investments will be negative. As bond investors know, there is an inverse relationship between bond prices and interest rates. As interest rates rise, the price of bonds will decline. In simple terms, the magnitude of the bond price decline is dependent on the maturity length of the bond or bond fund and the coupon yield for the bond.

Fidelity recently published a research report showing the impact on bond returns during one of the toughest periods for a bond investor: 1941 - 1981. During this stretch of time, intermediate treasury rates rose from .5% to over 16%. As detailed below, bonds that had higher rates tended to generate better returns over the early period of the '41 - '81 time period. The reason for this is bonds with higher coupons and or shorter terms returned cash to an investor sooner that could be reinvested at the then higher rates.

As mentioned earlier, the concern with the Fed moving to an increasing interest rate environment is the potential for an investor to experience negative total returns in the bond portion of their portfolio and many investors use bonds as an insulator or shock absorber to counteract volatile equity markets. I believe Fidelity's research article sums up the situation pretty well:

Investors have reason to worry about future prospects for bond returns—history shows that current low yields may be expected to result in below-average performance, especially if interest rates rise. Investors particularly concerned about the possibility of rising rates may want to diversify their fixed-income portfolios into less interest-rate sensitive sectors. However, the great bond bear market of 1941-1981 also offers some more comforting lessons as well. High-quality bonds are much less volatile instruments than stocks, and they do not lose that attribute during periods of rising rates. Even during a prolonged period of rate increases, owning bonds lowered the volatility and improved the risk-adjusted returns of an overall investment portfolio. As a result, investors may not look with much excitement at the near-term outlook for bond returns, but that doesn’t mean they should over-react by shunning bonds altogether.

Of particular concern is record levels of

cash continue to pile into bond funds as reported by ICI. The previously reference link also shows investment flow activity after the flash trading market correction from a few weeks ago. In aggregate, investors have withdrawn large sums of money from all types of investment funds, with the largest dollar amount coming out of equity funds. subsequent to the flash trading event. The

Zero Hedge website contains a chart of the S&P index graphed with the fund flow data.

For bond investors, pay attention to the maturity (better yet, duration) of the bond or bond portfolio. Additionally, staying invested on the shorter end of the bond curve could minimize the impact that a rising interest rate environment will have on a particular bond or bond fund's price.

Source:

Perspective on the Potential Downside for BondsFidelity Management & Research Co.

By: Dirk Hofschire, CFA

April 23, 2010

http://personal.fidelity.com/products/pdf/perspective-potential-downside-bonds.pdf