If history is any guide, the recent Fed Funds rate cut will not be the only one in this cycle. Greg Donaldson of Donaldson Capital Management has further discussion on this point in a post titled,

Stocks Twelve Months After A Rate Cut. In addition to additional rate cuts being anticipated, he notes "stocks" are generally 12% higher twelve months after the first rate cut. Certainly, all stocks will not be higher over this time period. Taking this one step further, one can look at the S&P 500 Index sector returns in different Fed Fund rate cycles.

Michael King and Scott Martin of the University of North Florida provide some research into market sector returns in a paper titled,

Federal Funds Target Rate Changes and Sector Equity Returns (link to paper can be found at bottom of linked page). The study, published May 25, 2007, examines the return of the S&P 500 sectors for the period January 1, 1999 to May 11, 2005. This is a rather short time period; however, it does capture market action during a point in time when the Fed was announcing its policy actions immediately following a Fed meeting. Prior to 1994 the FOMC meeting results were made public 45-days following the FOMC meeting.

During the time period noted above, the FOMC met 54 times. Subsequent to the meetings, the following Fed actions were taken:

- 14 rate increase.

- 13 rate decrease.

- 27 no change in rate.

If reviewing the sector performance in both increasing and decreasing rate environments, the research concluded:

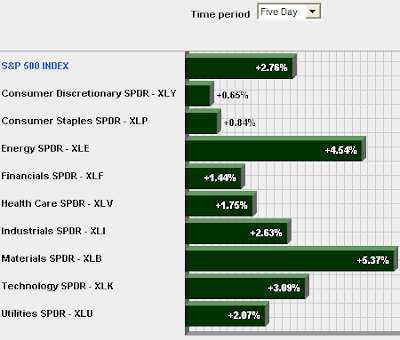

- on average, in a decreasing Fed Funds rate cycle, Consumer Discretionary, Technology, Materials, Health care and Financial sectors increased in value. The other sectors, Consumer Staples, Utilities, Energy and Industrials declined in value.

The research also looked at sector performance separately for increasing rate cycles and decreasing rate cycles. The table below summarizes some of the sector return data from the research. In order to read the table:

- In the "all cycles" column, for a 100 basis point (one full percentage point) decrease in the Fed Funds rate, consumer discretionary stocks rose 1.169%.

- In the "increasing rate cycle" column, for a 100 basis point increase in the Fed Funds rate, consumer discretionary stocks decline .446%

- In the "decreasing rate cycle" column, for a 100 basis point decrease in the Fed Funds rate, consumer discretionary stocks rose 1.49%.

(click on table for larger image)

The one surprising sector is the performance of utility stocks in a decreasing Fed Funds rate cycle. The research noted that utility stocks actually declined 1.454% for a 100 basis point decrease in the Fed Funds rate. This may be a result of the fact that the Fed cuts have generally come late in an economic cycle and take 6-9 months to have an economic impact. Consequently, the growth in utility earnings may slow early in the rate cut cylce as the economy tends to be slowing before the Fed does cut rates.