For the third quarter, S&P Dow Jones Indices is reporting that on a quarter over quarter basis buybacks for S&P 500 companies increased 14.5% and increased 3.7% on a year over year basis. The dividend plus buyback yield for the index is 5.53% and is at the highest level since the fourth quarter of 2011. The third quarter total of buybacks and dividends of $245.65 billion exceeded reported earnings of $205.90 billion. This is the fourth consecutive quarter that buybacks and dividends exceeded reported earnings. Highlights from S&P's buyback releases:

- For the seventh consecutive quarter, over 20% of the S&P 500 issues reduced their year-over-year diluted share count by at least 4%, therefore boosting their earnings-per-share (EPS) by at least 4%.

- Total shareholder return, dividends plus buybacks, set a 12-month record, at $934.8 billion.

- “...14.6% of the S&P 500 issues have a current share count level at least 4% lower than their Q4 2014 level, meaning that those issues have already front-loaded at least a 4% tail wind to their Q4 2015 EPS,” according to Howard Silverblatt, Senior index Analyst at S&P Dow Jones Indices.

|

| From The Blog of HORAN Capital Advisors |

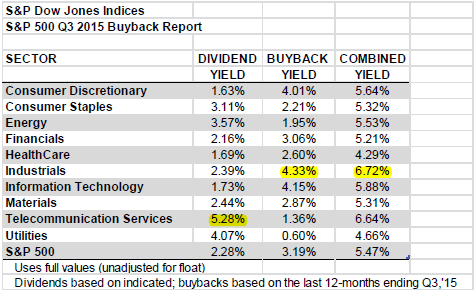

As detailed in the below table, the industrials sector has the highest combined dividend plus buyback yield of all the S&P 500 Index sectors at 6.72%.

|

| From The Blog of HORAN Capital Advisors |

It seems apparent that companies took advantage of the third quarter market weakness in the third quarter to reduce their share count. Historically, this has not always been the case as I noted in an article a few years ago; however, Q3 seems to be the exception.

|

| From The Blog of HORAN Capital Advisors |

One key to continued strength in buybacks and dividend growth will be the ability of companies to grow earnings and cash flow. Silverblatt noted in the report,

- Silverblatt stated that cash reserves declined 1.4% during the third quarter as S&P 500 Industrial (Old) available cash and equivalent decreased to $1.30 trillion, from the second quarter’s $1.32 trillion, and was 2.1% below the record $1.33 trillion set at the end of 2014.

- “High levels of shareholder return are now part of norm, with dividend increases almost assumed for non-commodity issues, and buybacks, while receiving bad-press, are expected to continue. Companies continue to have the resources to support these expenditures via cash-flow and still low financing rates. However, given that the Fed has now started to increase interest rates, debt financing will become more expensive, albeit slowly, putting pressure on buybacks. Cutting or limiting buybacks may not be a welcome move for investors, but scaling back dividends is typically a road that management avoids at high costs.”

Source:

S&P 500 Q3 Buybacks Increases 14.5% Over Q2 2015, Up 3.7% Year-Over-Year

S&P Dow Jones Indices

By: Howard Silverblatt, Senior index Analyst

December 21, 2015

No comments :

Post a Comment