One thing is certain and that is the markets have advanced significantly this year. The adage that a rising tide lifts all boats seems appropriate as it relates to many of the market indices this year. As a result and in hindsight, an index strategy would have served investors well in 2009. The Dow Jones Industrial Average (^DJI) has gained over 20%, the S&P 500 (^GSPX)over 24% and the Nasdaq Composite (^IXIC) over 45%. When looking at the market advance since the March 9th lows, the gains are even more pronounced; the DJIA is up 61%, the S&P 500 is up 67% and the Nasdaq is up 79%. This strong advance has pushed the index levels far above their 200 day moving averages.

|

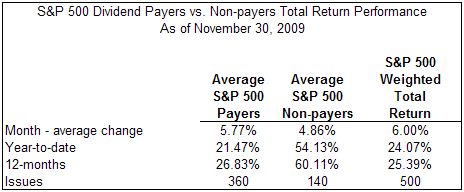

Source: Charles Schwab and Argus Research

As the above chart shows, P&G has generated a flat return on a price only basis versus a return in excess of 20% for the S&P 500 Index. As investors then, for 2010, look for opportunities in higher quality stocks that have not participated in this mostly lower quality stock rally of 2009.

As the above chart shows, P&G has generated a flat return on a price only basis versus a return in excess of 20% for the S&P 500 Index. As investors then, for 2010, look for opportunities in higher quality stocks that have not participated in this mostly lower quality stock rally of 2009.

Disclosure: Long Procter & Gamble

For investors looking at investment opportunities going into 2010, this likely means they will need to focus more specifically on individual stocks versus indexing. Even though the broader indexes are trading far above their moving averages, some individual stocks have not participated in the rally. For example, the below chart shows the performance of Procter & Gamble (PG) versus the S&P 500 Index (^GSPX).

(click to enlarge)

As the above chart shows, P&G has generated a flat return on a price only basis versus a return in excess of 20% for the S&P 500 Index. As investors then, for 2010, look for opportunities in higher quality stocks that have not participated in this mostly lower quality stock rally of 2009.

As the above chart shows, P&G has generated a flat return on a price only basis versus a return in excess of 20% for the S&P 500 Index. As investors then, for 2010, look for opportunities in higher quality stocks that have not participated in this mostly lower quality stock rally of 2009.Disclosure: Long Procter & Gamble