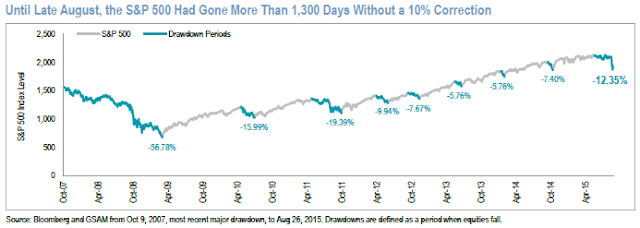

The equity markets have been anything but kind to investors long stocks. Nearly all the broad market equity indices are in negative territory for the year. The S&P 500 Index: -6.2%, Dow Jones Industrial Average: -8.5%, S&P MidCap Index: -4.4% and the S&P SmallCap Index: -4.6%. Simply reviewing social media comments from investors, one could be lead to believe the market has no where to go but down. Admittedly, the market trend and direction of least resistance does seem to favor the bears; however, some technical data is beginning to potentially signal a turn to a more bullish posture.

In August when the S&P 500 Index dropped to 1,867 the CBOE Equity Put/Call Ratio spiked to over 1.0 indicating a potentially oversold market. The market did recover from that August low, but recently has resumed its downtrend. Sometimes a better indicator is to look at the 21-day moving average of the put/call ratio. As can be seen in the below chart, the moving average of this ratio has begun to trend lower after reaching a high of .79 on 9/18/2015. Declines in this ratio are generally associated with a market that trends higher on a go forward basis.

|

| From The Blog of HORAN Capital Advisors |