What surprises me the most on this day after the election is the outpouring of advice pundits are freely offering to President Obama on how to deal with the current state of our economy. Following are just a few comments from today.

I surmise many pundits feel compelled to offer their advice to the President since they likely believe they did not hear concrete and credible solutions to dealing with the country's current fiscal predicament during the campaign leading up to Tuesday's election. This seems hard to believe since the two

candidates spent over $1.6 billion on this election. In hindsight, the voters have told Governor Romney they did not hear or believe his solutions either. This is some of the uncertainty the market is trying to digest. Although the election has come and gone, the uncertainty surrounding the fiscal cliff and debt ceiling debate will likely weigh on the market.

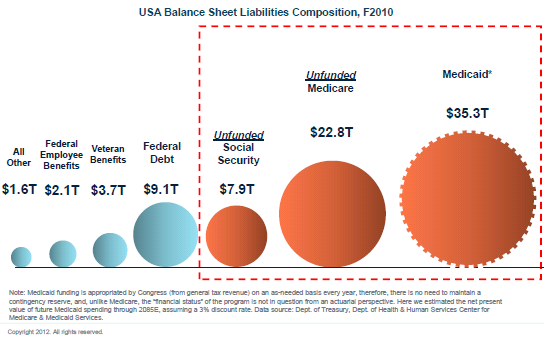

Ignoring the political party divide and looking at the state of our economy from a purely financial perspective, it appears the country is on a very slippery slope. Many individuals in their prime working years will likely not be too impacted from all of this as compared to events that may face our children and grandchildren. As Mohamed El-Erian says in his letter to the President, "For the first time in a very long time, our nation faces the possibility of seeing our children's generation end up worse off than their parents." In short, he is saying living beyond ones means has consequences.

At the end of October the

Treasury issued a refunding statement and noted in the statement's last paragraph, "Treasury continues to expect the debt limit to be reached near the end of 2012." The debt ceiling has been reached again after it was just increased on August 2, 2011, when President Obama signed a deal he had negotiated with congressional leaders to increase the debt limit of the federal government by $2.4 trillion. But now, after only 15 months, almost all of that additional borrowing authority has been exhausted. The government has taken on an additional $2.4 trillion dollars in debt in just over a year. This is not a sustainable path to go down as a country.

The consequences of the the U.S. government's continued printing of money to support deficit spending, I believe, may very well be low or stagnant economic activity and higher unemployment. In the end though, investors will be able to make money in this environment, but it will be more difficult. As Warren Buffett once said though, "Be fearful when others are greedy and greedy when others are fearful." The foreseeable future may be a time where investors can really take advantage of this contrarian sentiment investment advice.