The sentiment readings released so far this month continue to be reported at levels weaker than those associated with stronger economic growth. The IBD/TIPP Economic Optimism Index is reported near the beginning of each month. In August, the TIPP Economic Optimism Index declined by 5.6 percentage points to a historic low of 35.8 vs. 41.4 in July. The index is 8.6 points below its reading of 44.4 in December 2007 when the economy entered into its last recession. Index readings above 50 indicate optimism; below 50 indicate pessimism. The TIPP Index does a fairly decent job forecasting other sentiment reports released later in the month.

|

| From The Blog of HORAN Capital Advisors |

The TIPP Index is comprised of three components, all of which declined in August:

- The Six-Month Economic Outlook: a measure of how consumers feel about the economy’s prospects in the next six months.

- The Personal Financial Outlook: a measure of how Americans feel about their own finances in the next six months.

- Confidence in Federal Economic Policies: a proprietary IBD/TIPP measure of views on how government economic policies are working.

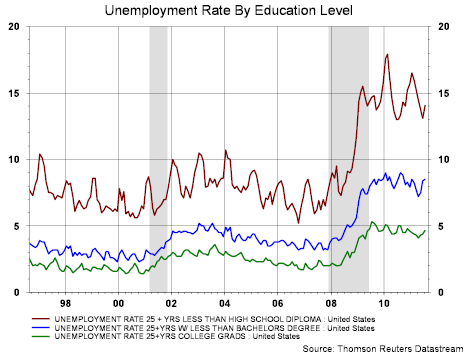

Of the 921 adults/households surveyed nationally this month, 29% of households say that at least one member of the household is looking for a full-time job. The economic policies to date have certainly not created jobs.

|

| From The Blog of HORAN Capital Advisors |

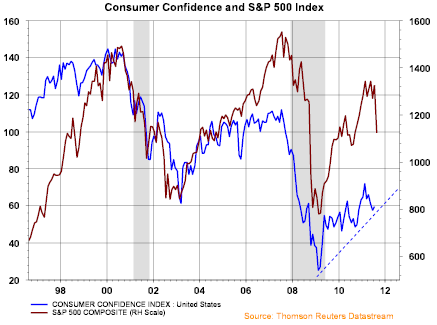

The consumer sentiment index released this past Friday was reported at 55.7 which was below expectations of 56, but, higher than the 54.9 reported in July. Tuesday the Conference Board releases its consumer confidence index. Consensus expectations are for the confidence report to come in at 52%. These levels are very depressed and far from an 80% reading that would be consistent with strong economic conditions. The importance of these sentiment and confidence figures is their correlation to consumer spending and more specifically retail sales.

|

| From The Blog of HORAN Capital Advisors |

Source: Barron's

Historically consumers have accounted for 70% of GDP and this deleveraging cycle is certainly influencing the consumer.

{kind=link}