An attractive aspect to using a dividend growth methodology in evaluating stocks is the dividend growth method enables an investor to gauge, indirectly, the cash flow of a company. Because cash is important to a company's survival, changes in a company's dividend practices may signal future cash flow issues for a company.

Dividend growth stocks should not be looked at as simply investments that grow their dividend on an annual basis; but, the methodology leads to investment in companies that are growing their business as evidenced by growth in company cash flow. The other important aspect to successfully investing in dividend growth companies is to focus on the higher quality firms as rated by Standard and Poor's. S&P's Quality Ranking measure attempts to capture the "quality" of earnings issue.

What is cash flow versus earnings? Earnings of a company are essentially a figure derived from accounting rules. The problem with "earnings" or "net income" from an accounting perspective, is the figure has very little to do with evaluating the cash flow stability of a company.

Cash flow comes in two forms: "operating" cash flow and simply cash flow. The latter is commonly referred to as EBITDA (earnings before interest, taxes, depreciation and amortization). The problem with the EBITDA calculation is the number is based largely on earnings. The website

stockdiagnostics provides the following interesting definition of EBITDA:

"(EBITDA) is calculated by adding "selected" expense items such as Interest expenses, Income taxes, Depreciation and Amortization back into earnings or net income. By adding "selected" expense items back into to a company's net income "more positive" earnings or cash flow per share numbers can be manufactured. When utilizing EBITDA an analyst or CFO is actually stating, "This is what our earnings would have been if it were not for interest, taxes, depreciation and amortization." Because it is based upon earnings, EBITDA is subject to the same "creative" accounting inherent in many earnings reports. EBITDA frequently does not reflect a company's true cash flow.... EBITDA is a manufactured "creative accounting" interpretation that presents a company in the best possible light. EBITDA's original use was for lenders to determine credit viability. Today these interpretations are used primarily by companies and Wall Street analysts to promote stock to an unwary public. Commonly, when EBITDA or CFPS (cash flow per share) are used in this way they are deceptively called "cash flow" or some form thereof."

Operating cash flow is a measure that incorporates changes from the balance sheet and income statement that have an impact on cash. The operating cash flow information is contained in SEC filings of companies. In the SEC financial filings for companies, firms include an income statement, balance sheet and statement of cash flow. One of the most important financial documents in the filing is the statement of cash flow. This statement reconciles the cash balance on the balance sheet by incorporating changes in categories from the income statement and balance sheet accounts. For example, all else being equal, if inventory increases, this reduces cash flow since cash was used to purchases the inventory. Of course, the inventory could be purchased on credit; then accounts payable would increase and this increases cash flow. The statement of cash flow contains three sections:

- Cash provided by operating activities,

- Cash provided by investing activities, and

- Cash provided by financing activities.

The key section to review on the cash flow statement is the one detailing operating cash flow.

Once the operating cash flow figure is analyzed, it should be converted to a per share number. This figure can be evaluated across quarters to determine any negative or positive trends. Additionally, growth, or lack of growth in operating cash flow per share can be compared to companies within the same industry or across industries. The last step in this analysis is to take the price of the stock divided by the operating cash flow per share to come up with a price to operating cash flow figure. This number can be used to evaluate stocks in the same way one uses the P/E ratio.

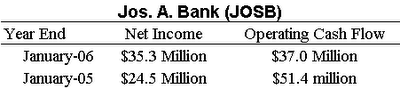

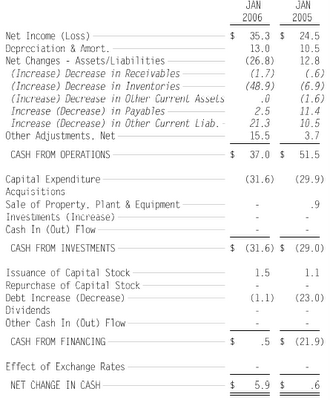

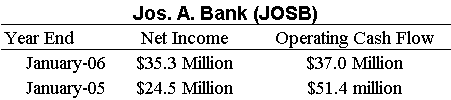

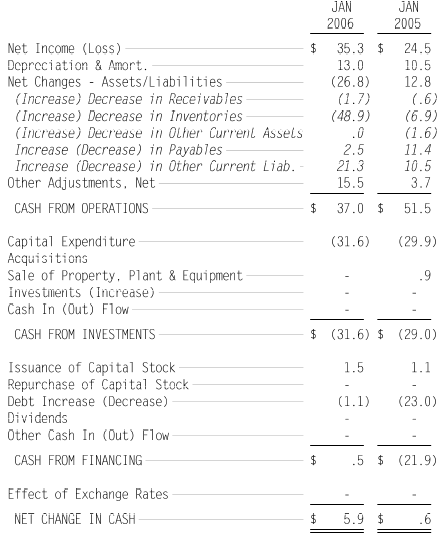

Following is an example detailing the difference in a company's net income and operating cash flow:

(click on tables for larger image)

Jos. A. Bank (JOSB) Cash Flow Statement

($ in millions)

As one can see from the above charts, net income has grown nicely, but cash flow has actually declined from year end '05 to '06. Note the large cash usage ($48.9 million) in 2006 attributable to an increase in inventory.

{kind=link}