There are times when I write a blog article and I remind readers the stock market and the economy are not the same. By that, I mean the stock market sometimes moves counter to what one might expect based on economic data releases. Often times this divergence occurs as the stock market is forward looking and its movement anticipates better or worsening economic conditions while much of the economic data is reporting on the past. Today however, it seems the market and economy are in sync to a certain degree. Since the S&P 500 Index low on March 23 it has returned over 53% on a price only basis as of the this past Friday. Over the last 24 weeks, the S&P 500 Index has generated a positive return in 16 of them with 8 weeks being down. Following is a review of some economic highlights which suggest many areas of the economy are improving in a 'V-shaped' manner.

In reviewing the August ISM Purchasing Manager's Indexes for Manufacturing and Services released last week, both are in expansion territory with readings above 50. As noted in the ISM report, this represents the fourth straight month of growth in the manufacturing segment of the economy. Additionally, the report notes, "demand and consumption continue to drive expansion growth." This is also reflected in the increase in the new orders component, as seen in the second chart below. Yes, the Services PMI ticked down slightly, but remains at a firm 56.9 in the August report and up from the low 40's in April.

The Census Bureau's latest report on retail sales is through July and shows retail sales now surpasses the high reached in January, before the virus mandated shutdown. Retail sales are up $123.2 billion from the near term low in April 2020. Clearly a 'V-shaped' recovery in retail sales.

This past week the Johnson Redbook report on retail same store sales noted a 4.6% YoY increase. This is a markedly better report than experienced during the shutdown and another variable showing a 'V-shaped' improvement.

Big ticket items like the sale of new light trucks and cars are rebounding strongly too. Light truck sales for August were reported at 11.6 million versus the 6.7 million level in April. Prior to the recession truck sales were near 13 million units.

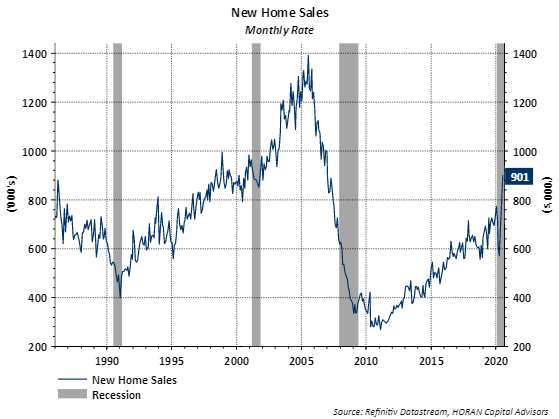

Another big ticker item is the purchase of a home. On a monthly basis, the sale of new homes is 130,000 units above the rate prior to the shutdown as seen below. The strong housing market has a positive multiplier impact on the overall economy due to the many other businesses that benefit from home purchases.

The strength in new home sales is also showing up in record NAHB Homebuilder Sentiment.

The existing home sale data below is shown on an annual basis and this to is above the pre-virus recession level. Existing home sales might even be stronger were it not for the low level of inventory in homes for sale.

One area of concern is the employment portion of the economy. This area seems to be improving at too slow of a pace. Jobless claims are clearly down from their near seven million recession peak, but 881,00 new claims remains too high.

Continuing claims are too high as well and include the 'Pandemic Unemployment Assistance' category, this totals 29 million individuals receiving some sort of unemployment assistance.

I noted in a report about a week ago that corporate earnings growth is expected to resume. The below chart shows that the I/B/E/S data from Refinitive is projecting 12-month forwards earnings growth of 9.6%.

For calendar year 2021 versus 2020, S&P 500 earnings are anticipated to increase 27.8%. The below table shows this growth broken down by quarter.

So the economic data is certainly strengthening and this is being reflected in corporate earning expectations. If this improvement continues, which I expect, all else being equal, this should draw more unemployed individuals into the workforce. Anecdotally, I see more job opening signs as I am out and about. Over the last 10 weeks, the S&P 500 Index has been up in eight of them. For all ten weeks, the market is up 13.22% so a little breather/consolidation is healthy and not necessarily a sign that the bull market run is coming to an end.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.