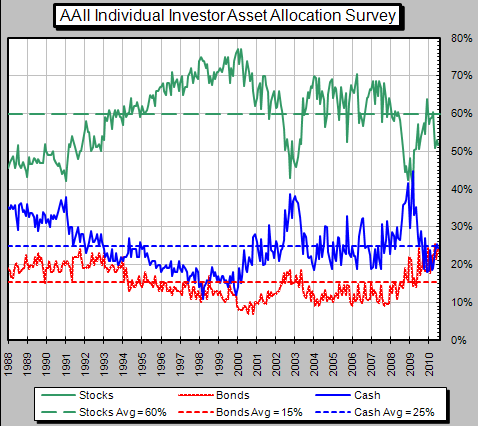

The world has changed. Market volatility is here to stay and increased correlations are making investors less reliant on modern portfolio theory. These higher correlations are likely the result of the globalization of trade, the introduction and adoption of new investment vehicles, and quantitative trading programs. The lack of diversifying properties within asset classes, particularly equity, has caused serious reservations among investors about future prospects. A recent Barron’s article commented that mutual fund flows from January 2008 to June 2010 has nearly $600 billion dollars moving into bond mutual funds while nearly $250 billion has exited equity funds (chart below).

Ramblings about bubbles forming in the bond market may have investors spooked but data would not suggest any near term outflows. Investors have opted for fixed income securities as more and more people become frustrated and disenchanted with equity returns. However, those same investors are starved for yield and now frequently reach to uncharted territory to satisfy income needs. Is lower quality or longer duration better? Which camp are we in, deflation or inflation? Is the double dip going to become a reality or is extended slow growth the next step? The common investor asks every day, “Where should I direct my investments?” Maybe he or she should be asking, “How do I invest to reduce overall market risks?”

Investors need strategy specific solutions which can provide consistent returns and hedge systemic risk. The environment for the past decade calls for such. The investment management community has heard those cries and responded quickly by providing alternatives in various wrappers: ETFs, ETNs, alternative mutual funds, structured products, and hedge funds. Clearly the adoption of these various vehicles has added to market variability but nevertheless, their intent is often times to provide hedged market returns within specific or multiple asset classes. These vehicles attempt to set predetermined return expectations. Some managers focus on absolute returns while others position for hedged but directionally long exposures. Regardless of which strategy, both intend to provide consistent and more predictable return streams.

Alternative investments, in their truest form, are unencumbered from trading constraints and provide intellectual freedom far beyond traditional money manager constraints. Example strategies: capital structure arbitrage, special situation events, long/short exposure, discretionary and systemic market trading. The global opportunity set truly becomes utilized as alternative investment managers act to expose market dislocations without traditional market boundaries. Alternatives are simply an expansion of an existing asset class or an investment intermediary between traditional asset classes to help facilitate acceptable balances between risk and return. Investors move between equity and fixed in a blurred or complimentary fashion via alternative investments. Managers must evaluate the means in which they assess market volatility relative to the fees they pay for risk-adjusted returns. For example, hedged equity has mostly long equity properties and should perform like long equity over a full market cycle but with significantly less market variability. Fixed income arbitrage and equity market neutral strategies should exhibit standard deviations equivalent to conservative fixed income securities as they hedge most market risk in an effort to achieve absolute returns conservatively higher than the risk free rate. A liquid alternative with compelling numbers in this category is the TFS Market Neutral Fund (

TFSMX).

In this type of economic environment, investors should be setting allocations to investment vehicles that answer the questions regarding how they will generate better risk-adjusted returns rather than where they will necessarily find them.